First Quarter 2011

Santa Barbara Real Estate Market Update

By Jackie Walters

Spring is here and March has brought a welcomed sense of renewal to the local real estate market, following a sluggish January and February. 135 residential buyers entered escrow in March, compared to 104 in February and 86 in January. The 135 pending sales in March represent four to five South Coast buyers per day writing deposit checks, signing contracts and showing continued confidence in investing in real estate. There were 143 pending sales one year ago, in March 2010, a difference of only 5.9% from last month's number, illustrating the fact that the market has now stabilized and the pace of sales activity is steady and sustained. Even our old friend appreciation is beginning to show its face in certain local entry-level sub-markets.

Let's do a little thumbnail retrospective on the local real estate market over the past several years. The pinnacle of residential real estate values, generally speaking, was in 2005. Most of us wistfully remember what our homes were worth at the "high-tide mark". It is said that "all real estate is local", in fact, as you will see, neighborhoods within a broader market can be on very different courses. Entry-level housing in Goleta and Carpinteria was the first market segment to stall in 2005. Foreclosures followed and bank-owned homes languished unsold month after month. The Santa Barbara market held its own from 2005 through the end of 2007 with a steady median price of around $1.2 million.

Montecito area values defied faltering neighboring markets and enjoyed an almost clockwork annual appreciation of 10% in its median and average price right through the end of 2007. 2008 saw a slow down in sales in the 93108 zip code and a plateauing in values. Following the financial meltdown, 2009 saw drastically reduced sales numbers in the high-end and a steep decline in prices. This was at the same time as sales in entry level homes, in Goleta, Carpinteria and certain Santa Barbara neighborhoods surged back to life absorbing the swollen inventory of distressed homes. Eager buyers took advantage of several government-backed incentive programs, as well as historically low interest rates. Enthusiasm for entry-level housing remains strong today both among cash investors and excited first time buyers. According to the California Association of Realtors, affordability, (the number of households in a community who can afford to buy an entry-level home), is at an amazing 58% -- up from a mere 14% in 2007.

Today's entry-level home buyers need to be prepared for what can be an emotionally draining process. Strong-willed buyers, however, are finding a pot of gold at the end of their journey. One local buyer shopped for over a year putting in various offers on short sales, foreclosures as well as regular sales. For various reasons, often due multiple offers or unrealistic sellers, his offers were never accepted. At times he would sit on the fence for weeks to "catch his breath". Just when he was about to give up on his dream, his Realtor found him a foreclosure property just as it was hitting the market for $417,000. He made an offer of $450,000 and it was accepted. (The very next day someone else made an offer of $500,000 but it was too late.) He has achieved his dream and couldn't be happier. Another couple, after being unsuccessful on 14 different properties, were finally the successful bidders in their 9th multiple offer situation.

The first quarter of 2010 saw a resurrection of the high-end market, with several significant closings in the first quarter over $8 million. Buyers are seeing alluring values everywhere along the South Coast. While activity remains focused in the under $1 million price range, we are seeing an increasing percentage of sales in the over $1 million market and throughout the upper price ranges. Motivated sellers with well-presented and well-priced homes, in all price ranges, will garner buyer attention and possibly even multiple offers. A chic and spacious downtown penthouse, listed for sale for $5,250,000, as unfinished space, just closed.

Table 1 shows a first quarter 2011 median price of $787,500 for houses and PUDs and $399,000 for condos. This is compared to $811,250 and $420,000 respectively for the same period 2010. There were 174 closed escrows for houses and PUDs in the first quarter, the same number as the first quarter of 2010. 66 condos sold in the first quarter of 2010 as compared to 53 condo sales for the first quarter of 2011. Contrary to the widespread notion that inventory numbers are bloated, the current inventory of active residential listings is down to 660 from 677 one year ago.

Table 1 also shows months-of-inventory, often referred to as "market velocity". This statistic illustrates how many months it would take to sell the existing inventory of homes, in a particular market segment, at the current pace of sales. Under 3 months of inventory is indicative of a seller's market; 3-6 months-of-inventory could be viewed as a balanced market; 6-9 months-of-inventory is a buyers' market and in excess of 9 months of inventory is a weak or soft market. Months-of-inventory market-wide for all price ranges and all neighborhoods, for condos, houses and PUDs, is 4.9 for March 2011. March 2010 had 4.7 months of inventory.

This month's headline is certainly in the months-of-inventory numbers for Santa Barbara and Montecito. Santa Barbara's 3.5 months-of-inventory for March 2011 is on the threshold of a sellers' market. 49 homes and PUDs entered escrow last month. Montecito's number of 7.7 months-of-inventory is close to half of the number of 13.5 for March 2010. 21 Montecito homes went into escrow last months vs. 13 for March 2010.

Table 2 compares the past year's closed escrow numbers by month to the 5 year average. An upswing in closings for the last two months of 2010 depleted results for January and February 2011; March has seen a nice recovery with 104 residential closings beating the 5-year average of 99 for the month. Sales pending for January through March remained strongly above the month's closed escrow numbers.

Table 3 illustrates the spread of closings by price range. While the bulk of the sales activity remains solidly in the $500,000 to $700,000 price range, you will also see a nice spread of activity in the upper ranges.

With the recession officially over in the summer of 2009, the first quarter of 2011 finds the South Coast real estate market in bloom. In her recent local presentation, Leslie Appleton-Young, chief economist for the California Association of Realtors, declared that "the worst is over" and "we are in recovery". She predicts a rise of approximately 2% in California's median price for 2011 and that coastal communities will lead the way. In our beloved Santa Barbara and surrounding areas, where one of the leading industries is the business of "residential living" the real estate market seems to reflect the promise of spring!

Showing posts with label Statistics. Show all posts

Showing posts with label Statistics. Show all posts

Sunday, May 1, 2011

Thursday, March 31, 2011

Months of Inventory - Santa Barbara Homes

Here are the current months of inventory for the Santa Barbara South Coast, (Carpinteria to Goleta), homes only, (not condos).

Months of Inventory, or Market Velocity, is the number of months it would take to sell all the current active listings, at the current pace of sales, assuming no new listings are added. To calculate this, we use the number of properties that entered escrow in the immediate past 30 days. This is a much better indication of buyer confidence today vs. closed sales that reflect buyer activity 2-4 months ago.

Months of Inventory, or Market Velocity, is the number of months it would take to sell all the current active listings, at the current pace of sales, assuming no new listings are added. To calculate this, we use the number of properties that entered escrow in the immediate past 30 days. This is a much better indication of buyer confidence today vs. closed sales that reflect buyer activity 2-4 months ago.

As a rule of thumb, 0-3 months of inventory indicate a sellers' market; 3-6 months indicates a "balanced market"; 6-9 months is a buyers' market and 9+ months is indicative of a weak market.

As of a few days ago, there were 479 homes for sale on the South Coast; 84 homes went pending in the immediate past 30 days, giving a market-wide rate of 5.7 months of inventory.

Breakdown by neighborhoods is as follows:

Carpinteria & Summerland: 7 mos of inv.

Montecito: 9.8 mos. of inv.

Santa Barbara: 4 mos. of inv.

Hope Ranch: 11 mos. of inv.

Goleta: 4.3 mos. of inv.

By price range:

$0-1 million: 3.1 mos. of inv.

$1-2 million: 6.8 mos. of inv.

$2-3 million: 8.1 mos. of inv.

$3-4 million: 16 mos. of inv.

$4-8 million: 7.7 mos. of inv.

$8+ million: 20+ mos. of inv.

One can see that the "hottest" segments of the market are the Santa Barbara & Goleta homes under $1 million; and the softest part of our local market is Montecito $8+ million.

Monday, January 31, 2011

2010 Year End Montecito Real Estate Market Statistics

Active Listings:

Last Year (2009): 573

This Year (2010): 575

% Change: 0%

New Listings:

Last Year (2009): 394

This Year (2010): 389

% Change: -1%

# Homes Under Contract:

Last Year (2009): 146

This Year (2010): 156

% Change: +6%

# Homes Sold:

Last Year (2009): 143

This Year (2010): 153

% Change: +6%

Sold Volume:

Last Year (2009): $492,534,075

This Year (2010): $540,101,644

% Change: +9%

Average Sales Price:

Last Year (2009): $3,444,294

This Year (2010): $3,530,076

% Change:+2%

The percentage of sale price to list price is remaining the same, hovering between 91-92% of asking price.

Last Year (2009): 573

This Year (2010): 575

% Change: 0%

New Listings:

Last Year (2009): 394

This Year (2010): 389

% Change: -1%

# Homes Under Contract:

Last Year (2009): 146

This Year (2010): 156

% Change: +6%

# Homes Sold:

Last Year (2009): 143

This Year (2010): 153

% Change: +6%

Sold Volume:

Last Year (2009): $492,534,075

This Year (2010): $540,101,644

% Change: +9%

Average Sales Price:

Last Year (2009): $3,444,294

This Year (2010): $3,530,076

% Change:+2%

The percentage of sale price to list price is remaining the same, hovering between 91-92% of asking price.

2010 Year End Graphs Depicting Santa Barbara's Real Estate Market

*These graphs show sales through the end of 2010 for all Homes/Estates in Santa Barbara South County (this includes Carpinteria, Summerland, Montecito, Santa Barbara, Hope Ranch, and Goleta).

Monday, January 10, 2011

Weekly Snapshot Statistics - Santa Barbara Real Estate Market

For the week of 1/3/11-1/9/11:

54 new listings

63 price changes

17 sales pended (12 under $1M, four $1-2M, one $4-8M) *29% over $1 million

20 closed (19 under $1M, one over $1M at $4,250,000)

24 off market (11 expired, 8 canceled, 5 withdrawn)

17 back on market

54 new listings

63 price changes

17 sales pended (12 under $1M, four $1-2M, one $4-8M) *29% over $1 million

20 closed (19 under $1M, one over $1M at $4,250,000)

24 off market (11 expired, 8 canceled, 5 withdrawn)

17 back on market

Thursday, December 30, 2010

More Santa Barbara Real Estate Market Statistics...

Here are some other useful numbers on the Santa Barbara real estate market (comparing 2010 to 2009):

Active listings: up 4.2%.

New listings: up 7.7%

Properties that went into escrow: up 8.2%

Sold properties: up 9.3%

Average sold price: up 6.9%

Sold volume: up 16.9%

Months of inventory remained consistent at approximately 8 to 9 months.

*Homes/Estates (These numbers do not include condos)

Active listings: up 4.2%.

New listings: up 7.7%

Properties that went into escrow: up 8.2%

Sold properties: up 9.3%

Average sold price: up 6.9%

Sold volume: up 16.9%

Months of inventory remained consistent at approximately 8 to 9 months.

*Homes/Estates (These numbers do not include condos)

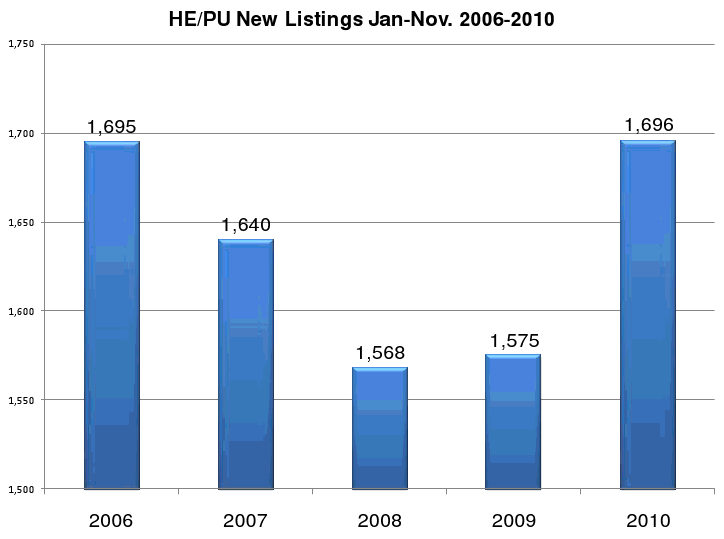

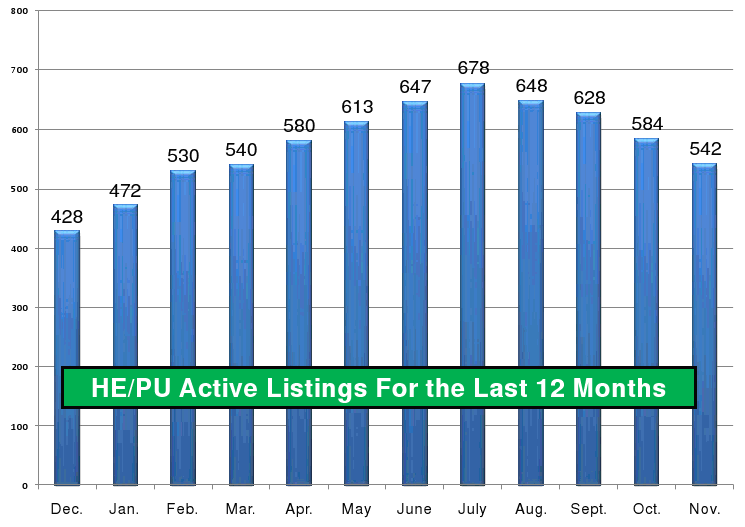

Visual Santa Barbara Real Estate Market Statistics

Here are some very resourceful graphs showing a picture of the Santa Barbara real estate market. These statistics were published through the Santa Barbara MLS on December 3rd.

He/PU=Home or PUD (Planned Unit Development)

CO=condo

All graphs run from the beginning of January through the end of November.

It's clear from these graphs that 2008 was our lowest performing year, we are seeing an uptick in the market, and prices are still low. There should be some good opportunities in 2011.

Sunday, October 31, 2010

Market Update - Through September 2010

Market Update (Through the end of September 2010 - Santa Barbara South County Real Estate)

**Statistics come out around the 5th of each month. October statistics will be out soon.

For the Home/Estate market (not including condos) through the end of September, the amount of sales declined compared to August. September showed 74 sales, and August showed 80 sales. Our median sales price went up, however, rising over $100,000 from $776,000 in August to $879,750 in September. The average sales price also went up substantially, rising from about $1.16 million in August to $1.57 million in September.

Looking by District: (Single family homes)

Carpinteria/Summerland

Sales are up from 52 last year to 55 this year, with the median sales price declining slightly from $687,500 last year to $662,500 this year.

Montecito

Sales are up from 105 in 2009 to 109 in 2010, and the median sales price dropped from $2.57 million last year to $2.41 million this year.

East Side of Santa Barbara

Sales are up almost 20% going from 156 in 2009 to 185 in 2010. The median sales price was $900,000 last year and is currently at $929,000.

West Side of Santa Barbara

Sales are also up over 20% from 114 last year to 142 this year, and the median sales price is up from $730,000 last year to $800,000 this year. It looks like that level of sales and prices should continue on the West Side with pended properties coming in at the same percentage as sales and the median list price on those escrows still hovering right around $800,000.

Hope Ranch

Sales are moving forward from where they were last year. We saw 10 last year, and we have 14 sales this year. The median sales price is also maintaining a lead over last

year when it was $2.175 million. This year those 14 sales have given us a median sales price of $2.675 million and an average sales price of $3.51 million.

Goleta South

There have been 79 sales this year compared to 61 last year, but the median sales price has declined slightly from $700,000 last year to $675,500 this year.

Goleta North

Sales rose from 115 last year to 123 this year, and the median sales price has gone up slightly from $703,000 last year to $710,000 this year.

Comparing September 2010 with its 74 sales and about $880,000 median sales price to

September 2009, we see sales down from the 85 of a year ago, but the median sales price is up from $750,000 last year to $880,000 this year. Essentially for the past 12 months the median sales prices have remained stable from month to month at around $850,000. There have been some peaks and valleys in this time frame, but the overall effect is that the median sales price for the area remains at around $850,000. The decline in the numbers of sales over the past 6 months can be attributed to 3 factors: 1) the end of the 1st Time Buyer Credit, 2) the usual seasonal slowdown and 3) the substantial numbers of foreclosures that we’re still being told are coming from the banks. If and when those foreclosures get released, sales will go up, but the median sales price could see a decline, since foreclosures tend to happen in the lower end of the marketplace, and this will shift the median, which is dependant on the bracket of homes that sell.

For the Condo market in September, sales went up to 23 rising from 22 in the previous month. The median sales price also went up rising from $427,500 in August to $460,000 in September. The average sales price rose from $507,027 to $529,538.

The Sales Price to Original List Price Ratio has remained strong for Condos all year hovering around the mid to low 90th percentile which means that when a property comes on at the right price, it goes out very close to that price. There have been 238 Condo sales through September 2010 compared to 226 at this time last year. The median sales price for 2010 of $437,000 is below the 2009 number of $467,000, but the median list price on the pended properties is $469,000 for both years. I think the disparity in the median sales price and median list price on the pended properties is due to the fact that most of those sub $400,000 condos are gone, so if something is going into escrow it’s higher up in the price range.

Looking at the Districts: (Condos)

Carpinteria/Summerland

The sales are up by about 30% going from 107 to 140. But, the median sales price has declined from $411,500 last year to $385,000 this year.

Montecito

Both sales and prices are up. For 2009 there were only 4 sales compared to 14 this year and the median sales price rose from $697,000 last year to $1,022,500 this year.

East Side of Santa Barbara

There have been 55 sales this year up from 43 last year, but the median sales price is down from $529,500 last year to $475,000 this year.

West Side of Santa Barbara

Sales are up, from 54 to 59 but the median sales price declined slightly from $510,000 last year to $495,000 this year.

Goleta South

Sales dropped by over 40% basically due to a lack of inventory. Last year there were 55 sales and this year there have been 38. The median sales price has also dropped from $453,000 last year to $370,000 this year despite a huge rise in the sales price to original list price ratio, which went up to 97.56%.

Goleta North

Sales have declined, from 38 to 30 for a 23% drop, but unlike Goleta South, the median sales price in the North has gone up from $375,050 to $408,500.

The decline in the numbers of Condo sales is much more pronounced when compared

to the drop in Home sales. Condo buyers would be the ones more substantially affected by the ending of the 1st Time Buyer credit and the numbers we see in this sector more closely resemble the numbers we see in the rest of the country for home sales. Just like with home sales, those three factors of 1st Time Buyer Credit, Seasonal Slowdown and the spectrum of more foreclosures about to be released is affecting whether people are going to buy or not.

Overall Santa Barbara is doing better than most of the rest of the country when you look at the Real Estate market. There is some uncertainty out there, which can make buyers feel timid. The results of the upcoming elections could resolve some of that insecurity, but there are still questions to be answered before we’ll see a big surge in both the number of units sold and a rise in the median sales price combined.

Monday, September 27, 2010

Mark Schniepp Speaks on the Economy

The outlook was focused mainly on commercial real estate, but Mark also covered the local and national economy, and local residential real estate. According to Mark, the recent drop in the unemployment rate is due to a "hangover" caused by the ending of census jobs and "not indicative of a second recessional dip." He says that jobs will recover and we will see job growth from here on out....just slowly, and that part of the speed of the recovery has to do with people and their behavior. Consumption is a large portion of our GDP and the amount that people are spending is down, due to saving more and changed financial circumstances. (I know I am one of them ... I have been much more conservative about my spending in this market. I see it in my clients too.)

Investors are looking for more certainty when they spend their money, and Mark counted real estate as a more solid investment for people to make & said he believes stocks will continue to put out a lower percent in returns over the next ten years. Real estate prices are expected to rise gradually. Compared to other locations in California, Sonia Fernandez wrote that "the South Coast real estate condition is somewhat protected, given location, constraints on growth, and what Radius Group Commercial Sales Principal Broker Scott Glenn called the "93108 effect" -- that is, Montecito-based investors who are taking advantage of the lower prices and investing cash in local real estate."

In terms of commercial real estate, "Downtown Santa Barbara is still king," according to Scott Glenn. Also, the students in the area are the reason why Isla Vista has the lowest vacancy rate of anywhere in the South Coast. The general vacancy rate for rentals (for the entire South Coast) is still only at 3-4%. This is also due to more people renting instead of buying at the moment.

Dr. Schniepp believes improvement is more likely to be visible by 2012, which is the same summary he gave earlier this year. (Earlier this year, he said 2010 will be better than 2009. 2011 will be better than 2010. And, 2012 will be better than 2011, etc.) He still believes there are some uncertainties out there that could impact consumer confidence and behavior, including the end of Bush-era tax credits, our health care system, and some energy policies that will impact the bottom lines of people and businesses ... but credit is starting to loosen which helps buyers and investors get back in the market. It was essentially the same news we've all been hearing. We are seeing improvement. It's just a gradual shift, and quite honestly, I think a gradual shift is the more sustainable thing we could ask for. It might not be sexy and full of instant gratification, but that's fine with me.

Feel free to share your thoughts!

Thursday, September 16, 2010

Weekly Snapshot Statistics - Santa Barbara Real Estate Market

For the week of 9/6/2010-9/12/2010

44 new listings

63 price changes

31 sales pended (22 under $1M, four $1-2M, four $2-4M, one $8M+)

*The number of sales over $1M is 27% for the week

16 closed

31 off market (18 expired, 7 canceled, 6 withdrawn)

3 back on market

44 new listings

63 price changes

31 sales pended (22 under $1M, four $1-2M, four $2-4M, one $8M+)

*The number of sales over $1M is 27% for the week

16 closed

31 off market (18 expired, 7 canceled, 6 withdrawn)

3 back on market

Monday, August 30, 2010

Weekly Snapshot Statistics - Santa Barbara Real Estate Market

For the week of 8/23/2010-8/29/2010

37 new listings

70 price changes

28 sales pended (18 under $1M, four $1-2M, four $2-4M, one $4-8M, one $8M+)

*The sale over $8M is 571 Sand Point Road, which is listed at $13.8M

*The number of sales over $1M is 36% for the week

21 closed

29 off market (11 expired, 12 canceled, 6 withdrawn)

13 back on market

37 new listings

70 price changes

28 sales pended (18 under $1M, four $1-2M, four $2-4M, one $4-8M, one $8M+)

*The sale over $8M is 571 Sand Point Road, which is listed at $13.8M

*The number of sales over $1M is 36% for the week

21 closed

29 off market (11 expired, 12 canceled, 6 withdrawn)

13 back on market

Saturday, July 31, 2010

Emily's Notes from Mark Schniepp's Economic Forecast

Below (meaning, two or three blog entries below) you can read the Newspress article dated July 9th, 2010, relating to Mark Schniepp's Economic Outlook that he presented at the Cabrillo Arts Pavilion on July 8th. The Newspress didn't share a great amount of data in their article, but I attended this event and was able to jot down quite a few notes and numbers, so here they are for you. Enjoy!

___________

Mark started by asking, "Why you should feel better about the economy and housing?" and followed up his question by stating: a) The recession is over, and b) Why aren't you convinced? I can't get a job.

(He says that our response mirrors the broader response.)

Mark stated that the recession ended in the first part of last year and that "data shows solid recovery but concerns remain." He always begins on a macro level, speaking to global and national issues, and then dives into data on the State of California and then specifically into Santa Barbara South County. (That's how these notes will be laid out as well.)

Mark stated there are mixed signals for the recovery, including housing. Housing starts are way down. The country lost 8.3M jobs in the recession. This is improving, but latest job creation has not yet mopped up the full size of the loss. Interest rates are the lowest ever, since we've been tracking them (beginning in 1971). The credit markets are the only thing limiting housing. Recovery is underway, although it is losing pop as the second half of 2010 arrives. Mark said that in recent news commentary, the weak reports are overstated. The workweek is lengthening in terms of hours across almost all sectors. which is creating stronger stream of income. There is greater confidence in economy. U.S. economic indicators clearly point to growth. We have surging stock profits and higher prices. Credit is moderating... Most lenders are no longer tightening their loan standards.

We are expected to have 3-4.1% GDP growth this year, but the GDP growth isn't high enough to mop up the unemployment rate. The higher unemployment rates will persist for an extended period, and will also prevent the Fed from raising rates soon. This will evolve the recovery into an expansion, and Mark states this is an important factor for a durable recovery.

California State will lag behind U.S. due to the budget. "It's broken!"

Commercial real estate is still weak. Business/Vacation travel is up. Labor markets are beginning to recover. Trade has risen sharply at world ports. We are seeing lots of exports. The Los Angeles film industry is up 25%. For California, housing sales have been strong since lows were hit 18 months ago. Even prices are rising. They are way off the lows, which were so exaggerated downward & influenced by distressed sales. They are 32% off the trough in California.

Notices of Default (or NOD's) are at the lowest level since 2007. We're seeing distress decline. What about the "shadow inventory"? Foreclosures were expected to rise but they're lower. More lenders are accepting short sales, altering principle, conducting loan modifications, and using other new solutions, as well.

Santa Barbara County:

The labor market is weak and the commercial real estate market is weak. The unemployment rate is improving, but there is not much job creation. We are also seeing more tourism but not enough to correct the jobs we have lost. Office vacancy rates are at about 14%, but Mark stated that this is still not bad compared to other areas. Santa Barbara Bank & Trust will probably survive and this saves 1000 jobs locally. Home sales are sharply higher in Santa Barbara South County.

Santa Barbara South Coast Real Estate (Single Family Residences):

With our number of sales, we are seeing a big improvement since last year.

By area:

Carpinteria +30.81%

Montecito +7.7%

Santa Barbara East +50%

Santa Barbara West +10.3%

Hope Ranch +42.9%

Goleta South +18.6%

Goleta North +12.7%

South Coast Overall +21.9%

The percent of sales over $1M is now at 38%, which is a great number. It was up to 60% at the peak of the market. The overall median price for the area increased 4.6% compared to 2009. The percent of sales under $800,000 is at 42%, and it hasn't been there since 2002 or 2003.

The origin of the buyer being from outside south coast hit the highest level since 2005. We are beginning to see investors enter the market again. We are also seeing more 1st time home buyers...the highest number we have seen since 2004 when we began to conduct surveys on where they buyers are coming from.

Condo sales are also up, and the inventory of condos is down, relative to where it was.

Here is our unsold inventory for homes:

$1M + = 16.3 Months

$750- 1M = 7.5 Months

$500-750 K = 4.3 Months

*You can see that the inventory goes way down as the price brackets go down. We have more inventory in the high end, specifically the $4M+ bracket, than we do in the low end of the market. We have 3.8 months of supply for California inventory.

Our median is currently $855k without Montecito and Hope Ranch. It is $911k if you include those two areas. This is higher than it has been for 12-18 months. Our median price for Montecito is currently $2,994,000, and the median price for condos is $458,000.

We do not have many short sales closing per month in S.B. County. We have roughly 6-8 sales per month. The same is true for REO (or bank-owned) sales. We have about 8-9 per month.

For the month of May, we had 6 foreclosures (1 in Carpinteria, 1 in Goleta, and 4 in Santa Barbara).

Summary

Homes are selling, especially cheap ones. Selling values have stabilized. Unsold inventory is low. There is virtually no new home building. Imbalances are growing. Home distress is down and foreclosures are in decline. A healthy market is waiting to emerge. Conventional recovery Q4 2010. Input observed by Q2 2011. It's coming, just slowly. 2010 is the transition year. Bumpy! It's why you feel the way you do. More convincing signs this quarter. Companies will begin hiring again.

Commercial Real Estate lags (as usual). State government will produce a drag. Interest rates are likely to rise from this point on.

Mark Schniepp, P.h.D.

California Economic Forecast

6489 Calle Real, Suite C, Goleta, CA 93117

Dr. Schniepp is currently Director of the California Economic Forecast in Santa Barbara. The Company prepares forecasts and economic commentary on the regional economies of California.

Thanks Mark! The next economic outlook will occur in September, and I will provide more data at that point. Feel free to call me at 805.252.2773 or email me at emily@villagesite.com for discussion.

___________

Mark started by asking, "Why you should feel better about the economy and housing?" and followed up his question by stating: a) The recession is over, and b) Why aren't you convinced? I can't get a job.

(He says that our response mirrors the broader response.)

Mark stated that the recession ended in the first part of last year and that "data shows solid recovery but concerns remain." He always begins on a macro level, speaking to global and national issues, and then dives into data on the State of California and then specifically into Santa Barbara South County. (That's how these notes will be laid out as well.)

Mark stated there are mixed signals for the recovery, including housing. Housing starts are way down. The country lost 8.3M jobs in the recession. This is improving, but latest job creation has not yet mopped up the full size of the loss. Interest rates are the lowest ever, since we've been tracking them (beginning in 1971). The credit markets are the only thing limiting housing. Recovery is underway, although it is losing pop as the second half of 2010 arrives. Mark said that in recent news commentary, the weak reports are overstated. The workweek is lengthening in terms of hours across almost all sectors. which is creating stronger stream of income. There is greater confidence in economy. U.S. economic indicators clearly point to growth. We have surging stock profits and higher prices. Credit is moderating... Most lenders are no longer tightening their loan standards.

We are expected to have 3-4.1% GDP growth this year, but the GDP growth isn't high enough to mop up the unemployment rate. The higher unemployment rates will persist for an extended period, and will also prevent the Fed from raising rates soon. This will evolve the recovery into an expansion, and Mark states this is an important factor for a durable recovery.

California State will lag behind U.S. due to the budget. "It's broken!"

Commercial real estate is still weak. Business/Vacation travel is up. Labor markets are beginning to recover. Trade has risen sharply at world ports. We are seeing lots of exports. The Los Angeles film industry is up 25%. For California, housing sales have been strong since lows were hit 18 months ago. Even prices are rising. They are way off the lows, which were so exaggerated downward & influenced by distressed sales. They are 32% off the trough in California.

Notices of Default (or NOD's) are at the lowest level since 2007. We're seeing distress decline. What about the "shadow inventory"? Foreclosures were expected to rise but they're lower. More lenders are accepting short sales, altering principle, conducting loan modifications, and using other new solutions, as well.

Santa Barbara County:

The labor market is weak and the commercial real estate market is weak. The unemployment rate is improving, but there is not much job creation. We are also seeing more tourism but not enough to correct the jobs we have lost. Office vacancy rates are at about 14%, but Mark stated that this is still not bad compared to other areas. Santa Barbara Bank & Trust will probably survive and this saves 1000 jobs locally. Home sales are sharply higher in Santa Barbara South County.

Santa Barbara South Coast Real Estate (Single Family Residences):

With our number of sales, we are seeing a big improvement since last year.

By area:

Carpinteria +30.81%

Montecito +7.7%

Santa Barbara East +50%

Santa Barbara West +10.3%

Hope Ranch +42.9%

Goleta South +18.6%

Goleta North +12.7%

South Coast Overall +21.9%

The percent of sales over $1M is now at 38%, which is a great number. It was up to 60% at the peak of the market. The overall median price for the area increased 4.6% compared to 2009. The percent of sales under $800,000 is at 42%, and it hasn't been there since 2002 or 2003.

The origin of the buyer being from outside south coast hit the highest level since 2005. We are beginning to see investors enter the market again. We are also seeing more 1st time home buyers...the highest number we have seen since 2004 when we began to conduct surveys on where they buyers are coming from.

Condo sales are also up, and the inventory of condos is down, relative to where it was.

Here is our unsold inventory for homes:

$1M + = 16.3 Months

$750- 1M = 7.5 Months

$500-750 K = 4.3 Months

*You can see that the inventory goes way down as the price brackets go down. We have more inventory in the high end, specifically the $4M+ bracket, than we do in the low end of the market. We have 3.8 months of supply for California inventory.

Our median is currently $855k without Montecito and Hope Ranch. It is $911k if you include those two areas. This is higher than it has been for 12-18 months. Our median price for Montecito is currently $2,994,000, and the median price for condos is $458,000.

We do not have many short sales closing per month in S.B. County. We have roughly 6-8 sales per month. The same is true for REO (or bank-owned) sales. We have about 8-9 per month.

For the month of May, we had 6 foreclosures (1 in Carpinteria, 1 in Goleta, and 4 in Santa Barbara).

Summary

Homes are selling, especially cheap ones. Selling values have stabilized. Unsold inventory is low. There is virtually no new home building. Imbalances are growing. Home distress is down and foreclosures are in decline. A healthy market is waiting to emerge. Conventional recovery Q4 2010. Input observed by Q2 2011. It's coming, just slowly. 2010 is the transition year. Bumpy! It's why you feel the way you do. More convincing signs this quarter. Companies will begin hiring again.

Commercial Real Estate lags (as usual). State government will produce a drag. Interest rates are likely to rise from this point on.

Mark Schniepp, P.h.D.

California Economic Forecast

6489 Calle Real, Suite C, Goleta, CA 93117

| mark@californiaforecast.com |

Thanks Mark! The next economic outlook will occur in September, and I will provide more data at that point. Feel free to call me at 805.252.2773 or email me at emily@villagesite.com for discussion.

Thursday, July 29, 2010

Mortgage Update

Mortgage Update Through the First Half of 2010

By Adam Black of Coast Village Lending, a Division of Prospect Mortgage

While we are still as an industry working our way through the challenges of the “Credit Crunch”, so far 2010 has brought many of positives. First, rates have been at historic lows at a point when most industry analysts were expecting them to go higher. As part of the 2008 Stimulus Act, the Fed was buying mortgage backed securities from Fannie Mae and Freddie Mac to the tune of $1.25 trillion.

At the start of 2010 the Fed started to slowdown and ultimately stopped their mortgage backed security purchase program by the end of the 1st Quarter of 2010. Without the Fed buying mortgages from Fannie Mae and Freddie Mac, the unanimous expectation was that their rates at would start to inch up. In fact, the opposite happened and we are now seeing conforming rates at all time lows.

Second, FHA financing continues to provide opportunity for more buyers to get into the market with little money down with loan amounts up to $729,750. Although the upfront mortgage insurance premium (the charge FHA adds to their loans as an insurance against default) increased from 1.75% to 2.25% FHA it is still a great financing option for buyers that otherwise may not have one.

Also, we have seen more use of the FHA 203k renovation loans. These loans allow buyers to finance home improvements into the purchase loan. Now, fixer properties become more of an option to first time buyers as they can use the renovation loan for anything from a new roof to new appliances, kitchen or bath. This loan can also be used by existing homeowners that do not have much equity, but would like get additional funds to improve their home.

Last, Jumbo and Super Jumbo financing is really starting to open up. Over the last few years Jumbo financing has been very difficult to find, and when we did find it, it was very restrictive. In the last six months we have seen the Jumbo loan market start to heat up. There are new products available, more investors offering Jumbo programs and extremely low rates. We now have a broad offering of well priced 5, 7 and 10 year ARM’s as well as competitively priced 30 year fixed loan options.

Written by Adam Black, Senior Loan Officer

Coast Village Lending, a Division of Prospect Mortgage

Adam can be reached at: 805-452-8393

By Adam Black of Coast Village Lending, a Division of Prospect Mortgage

While we are still as an industry working our way through the challenges of the “Credit Crunch”, so far 2010 has brought many of positives. First, rates have been at historic lows at a point when most industry analysts were expecting them to go higher. As part of the 2008 Stimulus Act, the Fed was buying mortgage backed securities from Fannie Mae and Freddie Mac to the tune of $1.25 trillion.

At the start of 2010 the Fed started to slowdown and ultimately stopped their mortgage backed security purchase program by the end of the 1st Quarter of 2010. Without the Fed buying mortgages from Fannie Mae and Freddie Mac, the unanimous expectation was that their rates at would start to inch up. In fact, the opposite happened and we are now seeing conforming rates at all time lows.

Second, FHA financing continues to provide opportunity for more buyers to get into the market with little money down with loan amounts up to $729,750. Although the upfront mortgage insurance premium (the charge FHA adds to their loans as an insurance against default) increased from 1.75% to 2.25% FHA it is still a great financing option for buyers that otherwise may not have one.

Also, we have seen more use of the FHA 203k renovation loans. These loans allow buyers to finance home improvements into the purchase loan. Now, fixer properties become more of an option to first time buyers as they can use the renovation loan for anything from a new roof to new appliances, kitchen or bath. This loan can also be used by existing homeowners that do not have much equity, but would like get additional funds to improve their home.

Last, Jumbo and Super Jumbo financing is really starting to open up. Over the last few years Jumbo financing has been very difficult to find, and when we did find it, it was very restrictive. In the last six months we have seen the Jumbo loan market start to heat up. There are new products available, more investors offering Jumbo programs and extremely low rates. We now have a broad offering of well priced 5, 7 and 10 year ARM’s as well as competitively priced 30 year fixed loan options.

Written by Adam Black, Senior Loan Officer

Coast Village Lending, a Division of Prospect Mortgage

Adam can be reached at: 805-452-8393

Recent Newspress Article on the Economic Outlook Presented by Mark Schniepp

Santa Barbara News-Press

SOUTH COUNTY REAL ESTATE MARKET ON STRONG REBOUND

STEVE SINOVIC, NEWS-PRESS STAFF WRITER

July 9, 2010 5:44 AM

South Santa Barbara County's residential real estate market has managed to tread the troubled waters of the economic downturn and is now making a double digit rebound.

That was the message delivered Thursday by economist Mark Schniepp, who gave a decidedly more upbeat mid-year economic update to 200 members of the Santa Barbara Association of Realtors at the Cabrillo Arts Center. He said home sales are up 22 percent from the same six-month period (January-June) of a year ago: 428 transactions. The median price, less Hope Ranch and Montecito, was $855,000, up 17 percent from last year's rock-bottom median of $730,000.

Like many other regions in California, "We're doing better than we did last year at this time," said Mr. Schniepp, principal of the California Economic Forecast. "Last year was completely different because many people were concerned about their day-to-day business operations and wondering if they would have a job.

Consumer confidence was very low and people were scared to make large purchases.

According to a survey conducted by Mr. Schniepp's office, about 30 percent of the home and condo sales in the first six months on the South Coast were to investors. "Certainly, some of these are people of means who are coming in to purchase second homes or rentals," observed Mr. Schniepp. "But we've also seen a lot of first-time home buyers taking advantage of lower prices, interest rates and tax credits -- especially for condos in the 400s.

Of the 400-plus transactions, Mr. Schniepp said 38 percent were over $1 million; approximately 42 percent were under $800,000. "We haven't had that many (in this price point territory) since 2002," said Mr. Schniepp.

That's where the market's hot right now.

Statewide, California median home prices are up 32 percent from the trough.

For those who can afford to purchase homes in south Santa Barbara County, Mr. Schniepp calculates about 25 percent of the transactions are cash sales. Those who need to acquire mortgages are finding tighter lending requirements where jobs, good credit scores, down payments and co-signers are part of the equation, even at the lower end.

Mr. Schniepp said potential home buyers now can secure a 4.57 percent interest rate on a 30-year mortgage. "That's a historical low compared to what it was 10 or 20 years ago,” he said.

But all the news he presented wasn't good.

While some may be ready to take the home buying plunge, South Coast residents, including many of the real estate agents present, aren't convinced the recession is entirely over, thanks largely to chronically high unemployment.

"It's not surprising you feel that way, but the recession ended a year ago," declared Mr. Schniepp, who displayed a dozen charts showing growth in key areas of the economy. "Unlike previous recessions, there are just so many fits and starts, especially on the jobs front," said Mr. Schniepp, who said the economy has managed to register three consecutive quarters of growth to its gross domestic product.

"We're seeing consumers spend again, but not in the numbers following earlier downturns. They are just tiptoeing back into stores.”

"The stock market is up 70 percent over the low, but we've seen some weaknesses and corrections lately, thanks in part to the dubious news about the European debt phenomenon that is weighing on (some) investors.

Will that contagion affect us? Mr. Schniepp believes, barring an unforeseen event, that it won't derail the U.S. economic recovery and push us into a double-dip recession.

The dearth of significant job creation is causing all the gloom, especially concerns of how the private sector will absorb 8.3 million Americans who lost their jobs in a brutal two-year period back into the economy. Complicating the recovery are 70 million Gen Yers, the cohort born after 1990, and looking to enter the job market.

"We haven't had this demographic phenomenon" in past downturns, said Mr. Schniepp, adding Santa Barbara labor markets are weak, and he doesn't predict any significant uptick until the end of the year and into 2011.

"The current year is a bumpy one, a transitional one," said Mr. Schniepp, echoing a sentiment from previous presentations. Signs of "a more exuberant expansion" will be felt in 2011 and 2012, when higher employment figures, continuing home sales and increased construction will be significant contributors to economic growth, said Mr. Schniepp.

For more information about Thursday's presentation, contact mark@californiaforecast.com

e-mail: ssinovic@newspress.com

SOUTH COUNTY REAL ESTATE MARKET ON STRONG REBOUND

STEVE SINOVIC, NEWS-PRESS STAFF WRITER

July 9, 2010 5:44 AM

South Santa Barbara County's residential real estate market has managed to tread the troubled waters of the economic downturn and is now making a double digit rebound.

That was the message delivered Thursday by economist Mark Schniepp, who gave a decidedly more upbeat mid-year economic update to 200 members of the Santa Barbara Association of Realtors at the Cabrillo Arts Center. He said home sales are up 22 percent from the same six-month period (January-June) of a year ago: 428 transactions. The median price, less Hope Ranch and Montecito, was $855,000, up 17 percent from last year's rock-bottom median of $730,000.

Like many other regions in California, "We're doing better than we did last year at this time," said Mr. Schniepp, principal of the California Economic Forecast. "Last year was completely different because many people were concerned about their day-to-day business operations and wondering if they would have a job.

Consumer confidence was very low and people were scared to make large purchases.

According to a survey conducted by Mr. Schniepp's office, about 30 percent of the home and condo sales in the first six months on the South Coast were to investors. "Certainly, some of these are people of means who are coming in to purchase second homes or rentals," observed Mr. Schniepp. "But we've also seen a lot of first-time home buyers taking advantage of lower prices, interest rates and tax credits -- especially for condos in the 400s.

Of the 400-plus transactions, Mr. Schniepp said 38 percent were over $1 million; approximately 42 percent were under $800,000. "We haven't had that many (in this price point territory) since 2002," said Mr. Schniepp.

That's where the market's hot right now.

Statewide, California median home prices are up 32 percent from the trough.

For those who can afford to purchase homes in south Santa Barbara County, Mr. Schniepp calculates about 25 percent of the transactions are cash sales. Those who need to acquire mortgages are finding tighter lending requirements where jobs, good credit scores, down payments and co-signers are part of the equation, even at the lower end.

Mr. Schniepp said potential home buyers now can secure a 4.57 percent interest rate on a 30-year mortgage. "That's a historical low compared to what it was 10 or 20 years ago,” he said.

But all the news he presented wasn't good.

While some may be ready to take the home buying plunge, South Coast residents, including many of the real estate agents present, aren't convinced the recession is entirely over, thanks largely to chronically high unemployment.

"It's not surprising you feel that way, but the recession ended a year ago," declared Mr. Schniepp, who displayed a dozen charts showing growth in key areas of the economy. "Unlike previous recessions, there are just so many fits and starts, especially on the jobs front," said Mr. Schniepp, who said the economy has managed to register three consecutive quarters of growth to its gross domestic product.

"We're seeing consumers spend again, but not in the numbers following earlier downturns. They are just tiptoeing back into stores.”

"The stock market is up 70 percent over the low, but we've seen some weaknesses and corrections lately, thanks in part to the dubious news about the European debt phenomenon that is weighing on (some) investors.

Will that contagion affect us? Mr. Schniepp believes, barring an unforeseen event, that it won't derail the U.S. economic recovery and push us into a double-dip recession.

The dearth of significant job creation is causing all the gloom, especially concerns of how the private sector will absorb 8.3 million Americans who lost their jobs in a brutal two-year period back into the economy. Complicating the recovery are 70 million Gen Yers, the cohort born after 1990, and looking to enter the job market.

"We haven't had this demographic phenomenon" in past downturns, said Mr. Schniepp, adding Santa Barbara labor markets are weak, and he doesn't predict any significant uptick until the end of the year and into 2011.

"The current year is a bumpy one, a transitional one," said Mr. Schniepp, echoing a sentiment from previous presentations. Signs of "a more exuberant expansion" will be felt in 2011 and 2012, when higher employment figures, continuing home sales and increased construction will be significant contributors to economic growth, said Mr. Schniepp.

For more information about Thursday's presentation, contact mark@californiaforecast.com

e-mail: ssinovic@newspress.com

Friday, April 30, 2010

Santa Barbara Real Estate Market Update - End of 1st Quarter 2010

Santa Barbara Real Estate Market Update - Through March 2010

Covering Santa Barbara, Montecito, Hope Ranch, Carpinteria/Summerland and Goleta for the Home Estate/PUD market, the number of sales rose from February, and the median sales price also came up. The median sales price has risen every month since January when it was $762,000. It hovered just below $800,000 in February, and landed at $890,000 in March. The average sales price remained at about $1,250,000 for February and March, falling from approximately $1.3 million in January. The sales price to original list price ratio also came up in March finishing in the high 80% range, which is excellent compared to about 75% back in January and about 70% in February.

Another big increase we saw in March was the number of escrows being opened. January escrows were in the low 50's, followed by February where we watched pending properties rise to about 65, but March showed that number at over 100. The median list price of those opened escrows was right around $880,000 in March. Inventory stayed about the same, and rose by less than 5% from February (around 550 homes for sale).

For the first 3 months of 2010 compared to the same period for 2009, the number of sales were up by about 20%. The median sales price came down slightly, from $822,500 last year to about $812,500 this year. The average sales price went up this year from $1,185,336 in 2009 to about $1,270,000 this year.

The condo market saw sales begin to rise in March, but the median sales price declined for the month dropping from $457,500 in February to $417,500 in March. The number of condos going into escrow also rose in March, coming up from 25 in February to 40 in March, but the median list price on those condos going into escrow fell from just under $500,000 in February to about $420,000 in March.

Comparing the first quarter of 2009 to the same period in 2010, the number of sales is way up, going from 36 last year to 65 this year (an 80% rise). The median sales price declined from $483,750 last year to $420,000 this year (a 13% drop). The number of escrows has gone way up with 91 this year compared to 62 in 2009 (a 47% rise).

The condo inventory did not come up substantially for the month of March, remaining in the low 140 range from Carpinteria through Goleta. The median list price of the inventory rose from just under $600,000 to about $630,000 during March.

Sales are starting to rise for the condo market as we move into spring, with about 1/3 of those sales in March arriving in the $500,000+ range. A big part of that rise is coming from Montecito, where we have 5 sales this year compared to none last year. The sub $300,000 range is also well represented with the median sales price for Carpinteria/Summerland and Goleta South still falling.

Wednesday, March 3, 2010

Weekly Snapshot Statistics - Santa Barbara Real Estate Market

Beginning the week of 2/22/10-2/28/10:

67 new listings

30 price changes

32 sales pended (22 under $1mm, seven $1-2mm, one $2-4mm, two $8mm+)

28 closed

29 off market (21 expired, 5 canceled, 3 withdrawn)

7 back on market

*We are beginning to see more sales particularly in the $1-2mm range, and more movement is happening in the higher price ranges as well.

67 new listings

30 price changes

32 sales pended (22 under $1mm, seven $1-2mm, one $2-4mm, two $8mm+)

28 closed

29 off market (21 expired, 5 canceled, 3 withdrawn)

7 back on market

*We are beginning to see more sales particularly in the $1-2mm range, and more movement is happening in the higher price ranges as well.

Tuesday, March 2, 2010

Update: Months of Inventory (broken down by price range and district)

Here is a quick little update on the months of inventory for the Santa Barbara South County Real Estate market.

Here is a quick little update on the months of inventory for the Santa Barbara South County Real Estate market.Carpinteria through Goleta (Homes & PUDs only, not including Condos):

Our total market has 610 active listings (not in escrow) right now, and this is trending up. In addition, we had 78 homes go "pending" in the last 30 days. This is also trending up. I think this trending up is normal, as we enter the spring and summer. This is the time when more sellers put their homes on the market and more buyers tend to be out looking. We currently have 8 months of inventory, which is steady.

Months of Inventory, broken down by price range:

$0-1mm: 4 months (steady)

$1-2mm: 7 months (this is down sharply & a great improvement)

$2-4mm: 22 months (steady)

$4-8mm: 48+ months (trending up - i.e. further weakening)

$8+ mm: 48+ months (trending up and further weakening here as well)

Months of Inventory, broken down by district:

Carpinteria/Summerland: 20 months (trending up - further weakening)

Montecito: 19 months (steady)

Santa Barbara: 5 months (steady & showing improvement)

Goleta: 5 months (steady)

*Hope Ranch: 5 months (trending down - good improvement)

*There are very few sales in Hope Ranch, and since the numbers are small, the months of inventory tends to fluctuate more than the other districts. One thing to note about Hope Ranch is that the 4 pending sales in the past 30 days have all been under $2 million. Some agents believe Hope Ranch has found its bottom.

Condos:

We have a total of 148 active listings, and this is trending up. We have seen 30 pendings in the last 30 days, so the number of sales has gone up sharply, and this is a good sign. The months of inventory is at 5 months, which is trending down and also a good sign.

Thursday, August 20, 2009

Weekly Snapshot Statistics - Santa Barbara Real Estate Market

For the weeks of 8/3/09-8/16/09:

95 new listings

96 price changes

77 sales pended

49 closed

68 off market (35 expired, 24 canceled, 9 withdrawn)

22 back on market

95 new listings

96 price changes

77 sales pended

49 closed

68 off market (35 expired, 24 canceled, 9 withdrawn)

22 back on market

Wednesday, July 29, 2009

Weekly Snapshot Statistics - Santa Barbara Real Estate Market

For the week of 7/20/09-7/26/09:

55 new listings

67 price improvements

29 sales pended (27 under $1M, seven $1-2M, one $2-4M, two $4-8M, two $8M+)

27 closed

34 off market (15 expired, 13 canceled, 6 withdrawn)

15 back on market

55 new listings

67 price improvements

29 sales pended (27 under $1M, seven $1-2M, one $2-4M, two $4-8M, two $8M+)

27 closed

34 off market (15 expired, 13 canceled, 6 withdrawn)

15 back on market

Monday, July 20, 2009

Weekly Snapshot Statistics - Santa Barbara Real Estate Market

For the week of 7/13/09-7/19/09:

53 new listings

58 price improvements

24 sales pended (21 under $1M, three $1-2M)

31 closed

33 off market (20 expired, 6 canceled, 7 withdrawn)

18 back on market

53 new listings

58 price improvements

24 sales pended (21 under $1M, three $1-2M)

31 closed

33 off market (20 expired, 6 canceled, 7 withdrawn)

18 back on market

Subscribe to:

Posts (Atom)